Beyond Business Intelligence

Predictive Science for Today's Bottom Line

Beyond Business Intelligence

Predictive Science for Today's Bottom Line

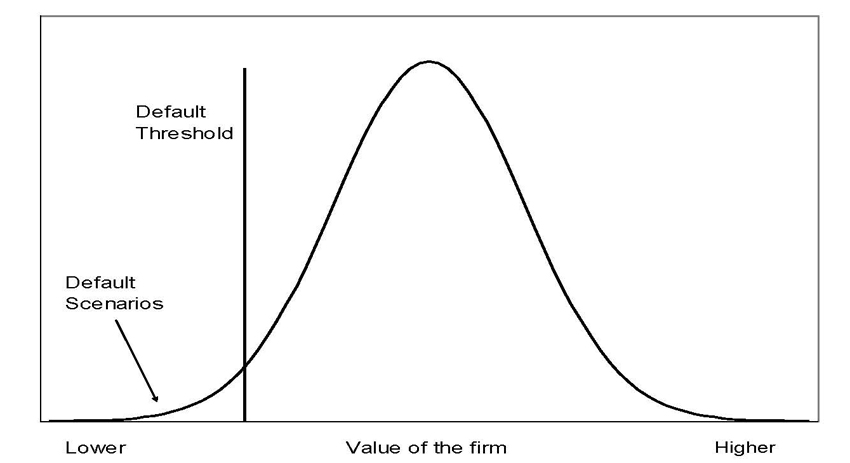

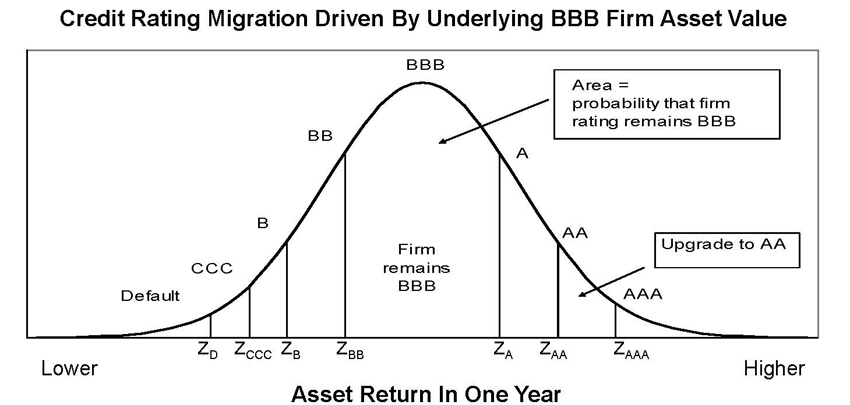

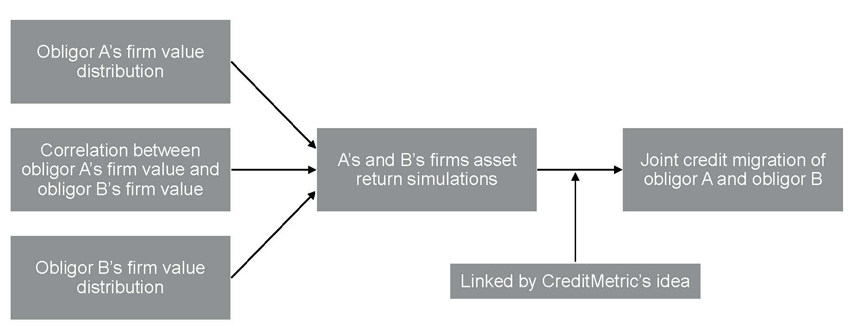

Credit risk is defined as uncertainty of value due to changes in credit quality. Credit risk in ERM is measured using the CreditMetrics approach which is based on the extended Merton model. Mertons insight was to recognize that the equity in a firm can be considered as a call option on the firms assets. As a result, the value of the firms debt can be expressed as the amount of liabilities outstanding reduced by the put option on the assets (the strike being the amount of liabilities). In this option theoretic valuation of debt, bonds become riskier if the return on the underlying equity is weakening, if the maturity is long versus short, if the volatility of the equity is higher rather than lower. The put option reduces the value of debt due to the possibility of default. This basic Merton model can be easily extended to include rating changes (see Section 3.2.1.4).

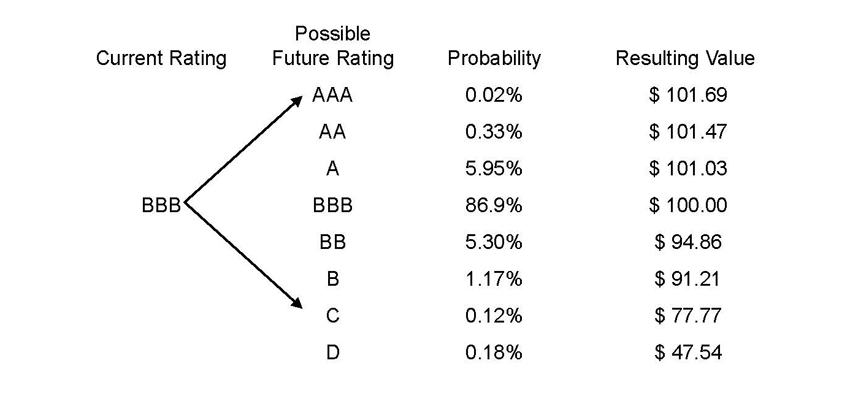

The Rating Transition Matrix summarizes the historical pattern of migration for bond ratings. For example, a BBB bond may be upgraded or downgraded with the following probability:

Given the range of possible values and probability, we can calculate the variance of the future value of a BBB bond

Mertons theory of the value of a Firms debt

Assumption: credit rating is driven by a firms asset value