Beyond Business Intelligence

Predictive Science for Today's Bottom Line

Beyond Business Intelligence

Predictive Science for Today's Bottom Line

|

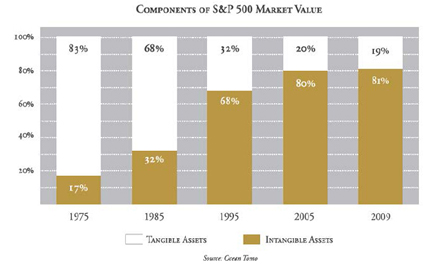

There has been an enormous paradigm shift in the past 25 years with respect to the nature of corporate assets. 25 years ago more than 80% of stock market valuations were supported by physical tangible assets (TA) with Intangible Assets (IA) supporting less than 20% of stock market valuations. Intangible Assets are assets that have value but that cannot be touched such as a brand, trademark, franchise, copyrights or patents. Intangible assets are largely comprised of intellectual properties (IP) and includes pre-protected IP (i.e., IP that has not yet been protected by patents, trademarks or copyrights). Today that ratio has completely flipped with intangible assets now supporting more than 80% of stock market valuations. In the past 30 years there has been an enormous transformation in the nature of commercial assets. This transformation has gone almost entirely unnoticed yet has extraordinary implications for all industry

In 1975 over 80% of stock market valuations were driven by tangible assets. Today that number has flipped so that less than 20% of stock market valuations are driven by tangible assets with over 80% being driven by intangible assets The implications of this paradigm shift are enormous. For one thing, intangible asset values have not historically been capitalized and entered onto corporate balance sheets at Fair Value (defined below) but have been expensed at cost through the profit and loss statement. Financial Accounting Standards Board (FASB) Opinions 141 and 142 now require that companies capitalize all intangible assets at Fair Value that are acquired in mergers and acquisitions (M&A) and assigned useful lives over which the intangible assets are depreciated. Goodwill (the difference between an assets market value and its purchase price) that has formerly been amortized over long periods of time (20 to 30 years) is no longer amortized but rather is subjected to an annual impairment test which may require that an assets value be written down. While these FASB rulings currently only apply to purchased intangible assets they nevertheless magnify the importance of standardizing valuation metrics between companies that are capitalizing intangible assets versus those that are not yet required to do so. The valuation and performance metrics between companies are practically meaningless if the valuation process does not standardize these values between companies. |

Also to be considered is FASB 157 that pertains to the Fair Value of an asset. Under FASB 157 companies financial reporting now requires that companies express asset values at their Fair Value which is defined as: The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. FASB 157 only applies to internally generated intangible assets if the assets can be reliably valued. FASB 141, 142 and 157 have arisen in order to provide shareholders with greater transparency largely in response to the paradigm shift in the nature of corporate assets and the huge variation in asset values attributable to intangible assets that also include Intellectual Properties (IP). The implication of the changing nature of corporate assets and the new FASB rules could not be greater for corporate managers and officers, investors and security analysts.

The three primary implications are: The second big issue is: And finally: |